A Comprehensive Guide to Climate-Resilient Home Loans and Green Property Financing

Let’s be honest. Buying a home has always been a leap of faith. But these days, the ground itself feels less certain. Wildfires, floods, and heatwaves aren’t just news stories—they’re real risks that can impact your property’s value, your safety, and your wallet. That’s where the idea of a climate-resilient home loan comes in. It’s not just a mortgage; it’s a financial tool built for the future.

Think of it like this: traditional financing looks at your credit score and income. Green property financing asks another question—how well will this house stand up to tomorrow’s climate? And more importantly, how can you use your loan to make it stronger, safer, and cheaper to run? This guide will walk you through the what, why, and how of navigating this new, essential landscape.

What Exactly Are Climate-Resilient and Green Mortgages?

Okay, first things first. The terms get tossed around a lot. “Green mortgage,” “energy-efficient mortgage (EEM),” “climate-resilient loan”—they’re cousins, but with slightly different focuses.

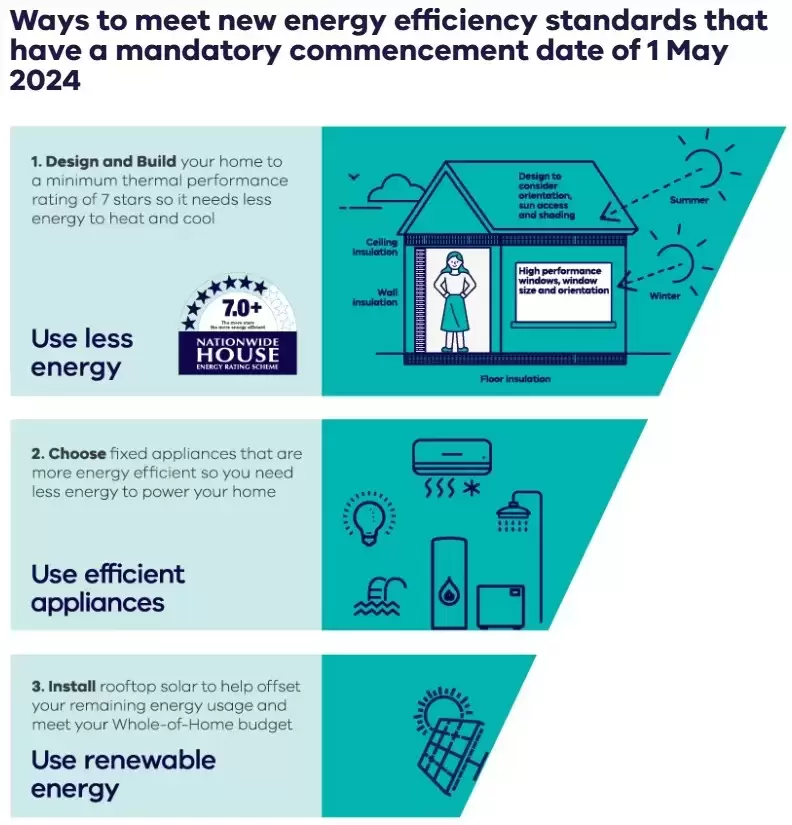

Energy-Efficient Mortgages (EEMs): The OG Green Loan

These have been around for a while. An EEM lets you borrow extra money to pay for energy upgrades—like new insulation, solar panels, or a high-efficiency HVAC system—by rolling the cost into your primary mortgage. The logic is beautiful: your total monthly payment might go up a bit, but your utility bills will plummet, often creating a net savings. You win, the planet wins.

Climate-Resilient Home Loans: The Next Evolution

This is where it gets really interesting. These loans consider physical climate risks—like flood zones, wildfire propensity, or extreme heat—and incentivize improvements that mitigate those specific dangers. We’re talking about fire-resistant roofing, upgraded drainage systems, impact-resistant windows, or even elevating a home. The goal is to protect the asset (your home) from devaluation and disaster.

In practice, the lines are blurring. The best financing options now often combine both: rewarding efficiency and resilience. Because a home that uses less energy is often better sealed and prepared for temperature extremes, you know?

Why This Matters Now More Than Ever

Sure, it feels good to be eco-conscious. But the drivers here are intensely practical. For homeowners and lenders alike, it’s about risk management.

For you, the homeowner, it means lower operating costs, increased comfort, and potentially higher resale value as “future-proofing” becomes a major selling point. Insurance premiums are skyrocketing in high-risk areas; a resilient home might help keep those costs in check.

For lenders, a home that’s less likely to be destroyed or depreciate is a safer investment. It’s that simple. They’re starting to see climate risk as a core part of their financial risk. This shift is what’s fueling new products and, sometimes, better rates.

Navigating the Financing Landscape: Key Options

Alright, let’s dive into the nitty-gritty. Where do you actually find these loans? Here’s a breakdown of the main avenues.

| Loan Type | How It Works | Best For… |

| FHA Energy Efficient Mortgage (EEM) | Allows cost of energy improvements to be added to an FHA loan without needing extra down payment. Based on projected savings. | Buyers using FHA loans for older homes needing efficiency upgrades. |

| VA EEM | Similar to FHA EEM, but for VA loans. Allows eligible veterans to finance improvements. | Veterans and service members purchasing homes that need green upgrades. |

| Conventional “Green” Loans | Offered by Fannie Mae (HomeStyle Energy) and Freddie Mac (GreenCHOICE). Provide financing for energy and water improvements. | Borrowers with good credit looking for flexible upgrade options on purchase or refi. |

| PACE Financing | Property Assessed Clean Energy. A special assessment on your property tax bill that pays for upgrades. Not technically a loan, but a key tool. | Homeowners who want no upfront costs and can handle a long-term tax lien. (Check local availability!) |

| Lender-Specific Programs | Some banks and credit unions offer their own green mortgage products with rate discounts or cash back. | Shopping around for the best local or personalized deal. |

Honestly, the biggest step is just asking. When you talk to a loan officer, don’t just ask about the rate. Ask: “Do you offer any energy-efficient or climate-resilient mortgage products?” Their answer will tell you a lot.

The Application Process: What’s Different?

Applying for green property financing isn’t a totally alien process, but there are a few extra steps. Be prepared for these:

- The Home Energy Audit: This is the cornerstone. A certified auditor will assess your home (or the one you want to buy) and produce a report detailing recommended upgrades and their projected savings. This report is your golden ticket.

- The Savings-to-Investment Ratio (SIR): Lenders will crunch the numbers. They want to see that the cost of the improvements is justified by the monthly utility savings. Usually, the savings must exceed the added mortgage cost.

- Using Approved Contractors: The work often must be done by licensed, and sometimes lender-approved, contractors. You can’t just roll in your cousin’s handyman discount (usually).

- The “Subject-To” Completion: For a purchase, the loan might close “subject to” the improvements being made within a certain timeframe after closing. The funds are held in escrow and released as work is done.

Beyond the Loan: Building Your Resilient Haven

Financing is the engine, but the upgrades are the journey. So what should you prioritize? It depends wildly on your location. A home in the arid Southwest has different needs than one on the Gulf Coast.

- For Wildfire Zones: Think ember-resistant vents, non-combustible roofing/siding, and creating defensible space. It’s about stopping the tiny, flying sparks that often doom homes.

- For Flood-Prone Areas: Elevating mechanical systems (HVAC, water heater), installing backwater valves, and using flood-damage-resistant materials below base flood elevation.

- For Extreme Heat: Cool roofing materials, advanced insulation, high-performance windows, and native, drought-tolerant landscaping to reduce the urban heat island effect around your home.

The point is to be strategic. Use your energy audit and, frankly, talk to your neighbors. They know what the real local challenges are.

The Bottom Line: A Shift in Mindset

In the end, climate-resilient home financing represents a fundamental shift. We’re moving from seeing a house as a static object to viewing it as a dynamic system—one that interacts with its environment and needs to be actively maintained for future conditions.

It’s not about fear, really. It’s about empowerment. Using the tools of finance not just to own a piece of land, but to fortify your shelter, reduce your long-term costs, and invest in a home that will be a safe, valuable asset for decades to come. The initial paperwork might feel like a bit more hassle, but the payoff—both monthly and for the long haul—can be profound. That’s the real deal.